May 2026

The Oil Market Was Left For Dead....

Not too long ago, the oil market was left for dead by investors. You could pick up oil companies at bargain-bin prices because it was perceived as a sector that would not grow. There was a never ending argument of supply vs demand. It seemed the world was awash with oil and demand would shift as EV’s were coming more into focus along with renewable energy sources. Both were going to change the world and fossil fuels were on the way out.

Or so everyone thought.

As someone who has always been invested in Canadian oil and gas companies, I didn’t believe the hype of a world where oil was no longer required. When COVID arrived and the market crashed in March 2020, it presented one of the best buying opportunities I had ever seen.

We were able to pick up some energy stocks at great prices - mostly pipelines - but a few E&P companies and have always actively followed the energy sector due to it’s large presence in the Canadian economy.

As you can imagine, we have been intensely watching the closure of the Strait of Hormuz, but what surprises me the most is that many people we speak to have no idea of the ramifications this event has, or most importably, will cause. In general terms, it’s cataclysmic.

This is the biggest energy crisis the world has ever experienced. It will trump (no pun intended) the oil embargo of the 1970’s, the financial crisis and COVID.

During the oil embargo of the seventies, rationing took place in many countries, including the U.S. To the naked eye, that seems like an unrealistic outcome of the current situation, but in reality, rationing has already begun.

For instance, airlines are cancelling flights in Asia and Europe, grounding planes and trying to mitigate the expense of high jet fuel as much as possible. Just the other day Air Transat announced a reduction of its flights due to the rising cost of fuel between May-October. Lufthansa, the German airline, cancelled 20,000 flights, and grounded some of their less fuel-efficient aircraft.

Airlines blame it on the price of fuel, which has definitely impacted their business, but it’s the lack of fuel that seems to be more problematic. They can cancel as many flights as they like, but if things play out as I suspect they will, there will be no jet fuel to be had. Airlines in Europe are currently trying to find suppliers to fill their summer requirements. Where does that supply come from? The U.S. can send jet fuel by way of tankers over to Europe, but that’s not going to come close to covering demand.

Canada also imports jet fuel from the U.S. so perhaps we aren’t as protected from this as we think.

If you have holidays booked for Europe this summer (like our family), you will likely see disruptions, if not full-on cancellations. I fully expect our flight to be cancelled, and if it isn’t, I debate whether to cancel it on my own. I do not want to get over to Europe and 3-4 weeks later find out there is no fuel or flights to get me home.

I know that summer is months away, but the damage has already been done. Just because the Strait opens tomorrow oil will not suddenly appear at Europe’s doorstep. Infrastructure has been damaged and reserves have been depleted. It will take some time to return to pre-war levels.

The paper and physical oil market have been out of whack for a while, but soon this spread will be gone and there will be no stopping the price of oil. Many investors are only now beginning to understand this scenario and as I always say, better late than never.

Oil investors know that one day the Strait will open and the price of oil will remain high despite that fact. Covid like lockdowns and work from home scenarios could be on the horizon in many countries. It will take a long time (years) for the world to return to pre-war levels.

The bull-run that investors have been waiting for in the oil patch is here, make sure you’re not sitting on the sidelines.

Income Taxes

It’s that time of year again when income taxes need to be filed and paid. I always find it interesting to see how pension splitting can impact our overall tax obligation. For the last two years, it was pointless to split our income, as we were worse off than if we didn’t. People assume it’s a much better result when electing to split income, but that’s not always the case.

It’s important to run the numbers.

Ours wasn’t a huge difference, but it did net us an extra $300 by not splitting.

We use Wealthsimple Tax. The platform is so easy if you have a simple tax situation (not self-employed or have a business). I’ve been told it’s like Turbo Tax or other similar tax filing software, but having it online with the addition of help when needed (for paid options) is super handy.

All the tax forms you receive from your employer and investment accounts are pretty easy to input, as you simply enter the amount for each box in the corresponding section of the Wealthsimple tax platform. It also has a great Help function where you can see the definition of each section, box or even see other questions that have been asked and answered. I actually think it’s pretty awesome and, quite honestly, worth paying for the upgraded options (we chose the $40 option).

In the past, we paid professional tax accountants a lot of money to help us navigate Canadian and U.S. taxes when we owned our Airbnb property in the U.S. Their guidance / support, and the ease of filing both CRA and IRS taxes from the same office was worth every penny we spent. Now that our tax situation is simple we don’t need to spend thousands of dollars for accountants to prepare our taxes for us.

I highly recommend you check it out if you prepare your own taxes using Turbo Tax or another similar program. You don’t ever need to download a program to your computer and I like that Wealthsimple is updated quickly with any new tax changes. It will also remind you of things that may have been forgotten.

RRSP/RRIF

Next time you speak to someone who is retired, ask them how they like the RRSP/RRIF. Usually you’ll hear them complain about all the tax they have to pay. That’s because over time that contribution they made 25 years ago has grown significantly. Deferring taxes sounds so appealing, until it doesn’t.

The government always wins in the end. All your contributions have years to grow and that larger balance will be withdrawn someday. It’s a good problem to have, I guess.

From personal experience, I can tell you it’s hard to deplete the balance in a tax efficient way. I invested a little over $20,000 about 25 years ago which has grown significantly. Once I stopped working at 49 before I began drawing my pension, I should have pulled out a good lump sum from my RRSP. I didn’t, and now I’m stuck trying to reduce the balance.

My goal is to cut my RRSP in half by the time I turn 60, but it’s tough. I realize now, I should have listened to my parents who tried to dissuade me from investing in my RRSP. Instead, I should have paid the tax on that $20,000 and invested in a non-registered account (there was no TFSA in those days). I was earning very little working part-time, while raising two kids, so the tax would have been minimal. But the person at the bank, and every book I read about investing, recommended the RRSP. Nothing has changed, in that regard, as they still recommend it over everything, even the TFSA.

I was thinking about this recently as I overheard someone complaining about their aging parent’s RRIF. Upon their parent’s death, as sole survivor, half the RRIF will go to the government. What’s worse, their parent never fully utilized their TFSA and are leaving unused contribution room on the table. All those years of saving and investing and the reward is paying the government half the account. I can’t imagine the people out there that have a similar circumstance. One thing is certain, the tax-man, or woman, will love them.

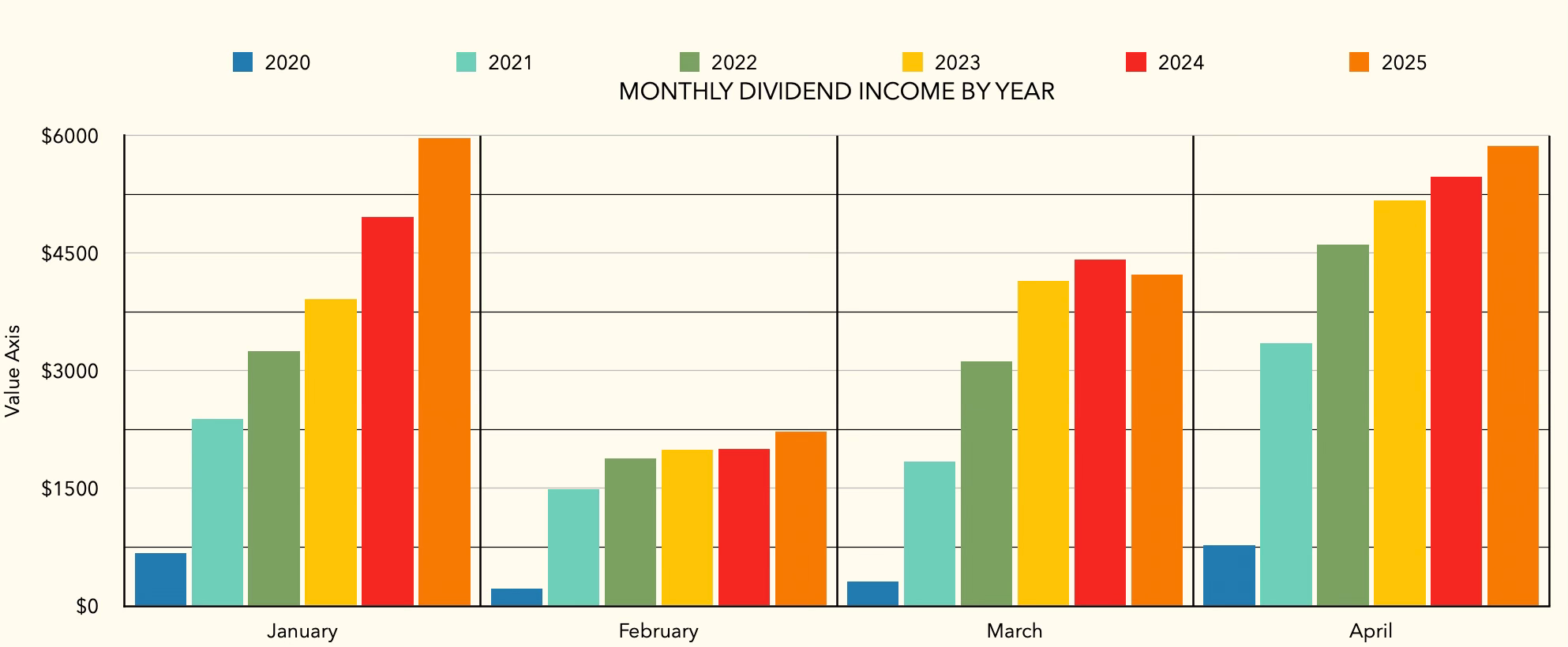

Our April Dividend Income

In April, we were just shy of earning $6,000 in dividend income which represents a 2% increase over the income earned in April 2025.

The following companies paid us this month:

Aecon

Alaris Equity Partners

Arc Resources

Bank of Nova Scotia

BCE

Canadian Natural Resources

Cardinal Energy

CES Energy Solutions

Dream Industrial REIT

Extendicare

Freehold Royalties

KP Tissue

Labrador Iron Ore

Peyto Exploration

Rogers Sugar

Sagicor Financial

Slate Grocery REIT

South Bow Corp

TC Energy

Toronto Dominion Bank

Wajax Corporation

Westshore Terminals

Whitecap Resources

Our forward annual dividend income is now over $53,000.

Transactions:

Unlike the previous months, April had some action. We sold our Aecon shares and captured a 173% gain. We also sold Extendicare at a 334% gain. We added some shares to our existing Trican Well Services holding and the rest of the money is sitting in cash waiting to be reinvested.

Beat the TSX

I was looking at the top highest yielding stocks on the TSX as of January 1st - the Beat the TSX list for 2026. These are showing a return of 8% YTD despite Telus and BCE still being in the negatives. You can see how the energy sector looks in this list, and how those oil/gas companies have helped to boost returns thus far.

Note: current price is from April 24th

I wanted to show you the Beat the TSX to reinforce the gains from the energy companies. The combined average YTD return for ENB, PPL, CNQ, and TRP according to my calculations above is 16.77%. Double the return of the 10 companies combined. The big winner is CNQ - a pure play oil and gas producer and likely the best managed company in Canada.

Currently the energy sector makes up 18% of the S&P/TSX Composite and is currently one of the top 2-3 sectors (financials being the biggest). But not long ago, it took up 35% of the composite during the last commodity-boom run of 2007/2008. At that time, oil prices surged to almost $140 a barrel and oil producers were making money hand over fist.

The lowest point for the energy sector came shortly after this boom, in 2015 and onwards, when oil was left for dead. During this period, the energy sector fell to roughly 10% of the TSX composite.

We are leaving that era behind us now, and I believe, like many others, that we are entering a period where the energy sector will regain its dominance within the TSX composite.

One final note to leave you with… here’s the latest from Amber Kanwar and it’s definitely worth a listen.

Nothing ever wrong with taking profits, but I’m confident Aecon is going to keep running. I have a huge chunk in my non-registered and need to avoid triggering capital gains until 2027. Expecting $60-$70 by then.